Robert has done extensive research since 1966 in an effort to understand why human beings are violent and has been a geopolitical analyst since 1971. Since becoming a nonviolent activist in 1981, he has been involved in many nonviolent action campaigns and been arrested for nonviolent acts of conscience about 30 times. He is the author of The Strategy of Nonviolent Defense: A Gandhian Approach and ‘Why Violence?’

Leading cryptocurrency lender and financial services firm BlockFi filed for Chapter 11 bankruptcy protection on Monday, becoming the latest company in the industry affected by the collapse of major crypto exchange FTX.

In the filing with the US Bankruptcy Court for the District of New Jersey, the company said it had more than 100,000 creditors, with liabilities and assets ranging from $1 billion to $10 billion.

“BlockFi looks forward to a transparent process that achieves the best outcome for all clients and other stakeholders,” stated Mark Renzi from Berkeley Research Group, which serves as BlockFi’s financial adviser.

Comment: By reading the comments in this post it is clear that the people are awake and aware; crypto is another fiat ponzi scheme backed by hot air; no different to the Federal Reserve System;

In the days to come, you will be hearing some odd phrases. One of them is “Sovereign” Debt Collapse.

This is a misnomer as most phrases involving the word “sovereign” are.

The guilty parties want you to think that such a thing as “sovereign” debt exists, and the rest of the people who use this phrase think they know what they are talking about —-like those who use the phrase “sovereign citizen”—- but don’t really.

In just one transaction, Prince Philip received $950 Trillion Dollars from the GOVERNOR of OTTAWA as payment for Life Force Value Annuities.

The entirety of world debt — all debt, governmental, private, and personal — amounts to $303 Trillion Dollars at the present moment.

So what is this nonsense about “sovereign debt collapse”? Obviously, Prince Philip left behind an estate more than competent to pay off world debt and have twice as much left over, based on just one transaction.

They will tell you, oh, it’s not that sort of sovereign debt.

But it is.

The guilty parties are trying to pin the tail on the sovereign people and nations of the world, instead of the Sovereigns responsible for this egregious situation.

What a “Sovereign Debt Collapse” actually means is that the Sovereigns are not paying their debts owed to the sovereign peoples and nations.

Remember Joe and Andy?

(1) Andy walks in, hands a $10 I.O.U. to Joe and Joe gives him a hamburger.

(2) Joe’s hamburger has paid for Andy’s debt.

(3) Now Joe and Andy are both in debt. Joe is in debt to himself, because he is bearing the loss of his labor and materials to create the hamburger, and Andy is in debt to Joe because he never actually paid Joe.

(4) Because there is no end date to this transaction, Joe can’t force Andy to pay.

(5) The debt of Andy to Joe thus becomes a debt of honor, and the only thing proving that a debt exists, is the Note.

(6) The same circumstance applies to every such transaction, big or small, that occurs under the same conditions: that is, debt offered as payment, actual goods and services exchanged for debt, no date established for payback.

They are turning their Royal pockets inside out and pretending that they are skint, and furthermore, pretending that they don’t know who their Creditors are— while they are busily killing their Creditors to avoid payment of their Sovereign Debt (Government Debt) to the actual sovereign people of each nation.

So whether it is an actual “Sovereign” like Queen Elizabeth’s brood, or a Government Corporation standing in the place of such a Sovereign, the story is the same.

They have the money (actual assets) in their control, because they took (false) title to all the assets, and they have the credit (as debt notes) in endless supply— because they run the printing presses — and because there is no set date to repay the people, they stand around and say, “Well, not today….my big toe aches. It’s inconvenient. I have a bet placed on the Ukraine War and might have to pay up…. You know how it is….”

Simple enough, isn’t it? This is what they always do, century after century. They use the sovereign people and their assets as collateral to borrow credit from the banks, and when the credit can’t be supported anymore, they kill their Creditors.

They don’t have to pay back the credit to dead people, they get to keep the remaining assets — land, gold, silver, etc., that they purloined under color of law and authority that they don’t actually have, they get paid to clean up the mess they made, and tax the survivors to rebuild everything they destroyed.

So why not kill millions, even billions of innocent people, using a Snake Oil Hoax and coercion?

The Life Force Value Annuities Prince Philip received in April of 2017 are insurance policies on insurance policies that prepaid Prince Philip for the deaths that are occuring now — which makes no sense until you realize that insurance is nothing but legalized gambling.

Prince Philip sold off his “assumed” interest in all the livestock in the United States and Canada; in his view, and the bank’s, that included the people living here. He collected the life insurance annuities as part of the payoff when he sold his ownership interest. You can’t insure something if you don’t have an ownership interest in it, so….

China bought that presumed-to-exist ownership interest, and has been busily telling Joe Biden what to do ever since. The same thing occurs when corporations change hands in other fields — if Ryobi buys out Lubbock Tool and Die, the Lubbock brand may remain in evidence, but all the decisions about the company in Texas are now being called by a Japanese Board of Directors.

All this is part of the Vermin’s long term plan to move their center of business to China.

Of course, it was all very quiet, no big announcement, but you can hardly move $950 T in a world economy where the accumulated is $303 T without causing a few waves in the bathtub.

Thus, we do have compelling though circumstantial evidence that Prince Philip knew what was coming, and that he was in on it, Big time. Other things like his famous statement that he wanted to come back from the dead as “a loathsome virus” also adds fuel to the circumstantial evidence, as does the decision to sell out his purported North American interests in 2017, just prior to a giant infusion of Royal Cash Assets into HSBC.

I would say that Philip was loathsome enough whatever package he came in, but there is little doubt that he continues to haunt our days right now.

Now, notice who paid him? The GOVERNOR of OTTAWA, that is, the Municipal Corporation “Governor” of the Municipal Corporation of Ottawa, which is an independent international city-state just like Washington, DC, just like Vatican City, just like the Inner City of London, just like the United Nations, just like NYC.

These things have proliferated like putrid ulcers all over the Earth, little Municipal City-States bound under the Roman Civil Law, all theocracies owing tribute to the Roman Pontiff — and it really doesn’t matter what they call the “Papal Bridge” these days. They pretend that Papal Office is closed, but the crime syndicate and the modus operandi remains the same.

Whether you call a Pope a Pontiff or a Pontiff the Pope, the man wearing the hat remains the same. Call me late for supper and things get serious; otherwise, what offices the Pope occupies and what those offices are named, remains a game that the Pope plays without any obligation to tell you or me.

What the Pontiff, or “Papal Bridge” does, is to provide money and banking services of extraordinary kinds, like cashing out Prince Philip and loaning gold to China to do it. Now you know who has been financing and directing the whole move to China for the past thirty-plus years, and we know this is true, because the GOVERNOR of OTTAWA who paid Philip was an aged Catholic Archbishop suffering from cancer, who died soon after this transaction was completed.

Think about it. The Church has been collecting income taxes from the serfs since 1135 A.D. The only change is that we pay a much larger percentage of our earnings than the serfs did. Even what they use the tax money for remains the same: crusades, “holy” war, as if war were ever holy.

Remember Voltaire’s quip about the Holy Roman Empire — that it wasn’t holy, wasn’t Roman, and wasn’t an Empire. We could all say the same about the present situation if we were half as observant as our ancestors.

So, the “Royals” are busily killing off their Creditors for cause. They hate owing people money that they are morally obligated to pay back. It doesn’t suit their Royal whim to be in “uncertain debt” to the great unwashed masses who look to them for wisdom and care and guidance, like children mistaking Satan for their kindly Grandfather.

And things are about to get worse, not better.

You might ask how things could possibly get worse? It will get worse because the militaries of the world woke up and began killing off the Royals and all their minions for their many crimes against humanity.

Kill some of them and some members of Congress, purely as scapegoats, and gin up a “war” with China to kill a few million Chinese (more Creditors gone) —hey, from the military’s standpoint, this has been a perfect set up.

They get everything that they want: scapegoats, control of the assets and credit, and a relatively “good” excuse to go after China and retrieve more of the gold and credit the Royals pilfered and which the Chinese borrowed from the Pope.

Remember kindly that all the things these guys are playing with ultimately belong to you and me and the other equally innocent people who stand to die in Shanghai and Peking.

And by the way, the “Open Borders Policy” makes perfect sense.

The American Creditors are being killed by the Snakeoil Hoax, and the Hondurans and Mexicans and Guatemalans are being brought in to replace them as debt slaves. That’s why the illegal immigrants are specifically exempted from having to drink the Kool-Aid.

The Royals, and now the militaries, don’t owe the South Americans very much and South American lives are not worth much in their scale of things, but the moment they cross the border and can count as “American Assets” these people grow tremendously in value as presumptive inheritors of the various Public Trusts.

These “new Americans” can act as place-holders in the Public Trust Scheme and this will allow the Perpetrators to retain control of all their yummy Slush Funds.

All of this is proving to be a great temptation to the militaries that are involved in the so-called Clean Up.

There are numerous Generals and Admirals who see this as a chance to rule the world behind figurehead politicians — but wait, that’s what they have been doing here since 1863 — and the only thing preventing them from continuing would be public awakening on a worldwide scale.

Which is happening.

It’s almost comical. While they fizzle-fart around standing on first one leg and then another, wondering what kind of narrative they can sell to the ignorant Public, Rome burns.

A strange paralysis has set in, a sort of Three-Way Standoff between those who wonder: “But if we tweaked this just a little bit, we might be able to pull it off….” and those who have very clear visual memories of nooses and Les Miserables, and a third group who actually do have a sense of patriotism and honor.

Just like the Angels in Heaven, it’s a three-way split, with one-third going the way of Satan, and two-thirds remaining on the side of God.

So Sydney Powell isn’t wrong when she says, “It’s Biblical.”

There is also very little doubt which side will win the toss up, so long as we all do our parts in the civilian world.

Doing our part means committing full devotion to Rat Watching and Rat Reporting — sharing the information is of critical importance and dissing the Mainstream Media is, too. People need to know, for sure, that the Media Talking Heads are completely, 100%, and literally —owned. This serves three desperately needed purposes: (1) it keeps the militaries honest and (2) keeps the Public informed about what we are up against and (3) it breaks the power of the media brain-washing operation.

Does anyone think that it is a coincidence that the BBC’s motto is: “Listen and obey”? Millions upon millions of innocent people have listened and obeyed and day by day they are paying the price. It’s time that the media moguls and Talking Heads were given The Turning Knob.

All the Spanish and French-speakers among us need to take on an extra burden to explain the situation to the would-be new immigrants from South America, who, having suffered more than we have in this country, will more rapidly understand how they are being used by these Democrats working for China, and the fate that is planned for them here in the “Land of the Free”: debt slavery and store-fronting for evil, by any other names.

Here are two exceptionally insightful presentations that you should all watch and study, and share widely —

It’s apparent that many people are confused and not quite getting my comments about the banking system as a pipeline operation and are frustrated and confused about the current situation where we have come so far toward our own banks and still don’t have them doing what they need to do.

The current bank transfer system in the West was “engineered” by John D. Rockefeller. His sons updated it as “the Swift System”. It has been the means that banks transfer credits and debits for decades and it is little more than a fancy FAX system.

J.D. Rockefeller is most famous as a Nineteenth Century robber baron and oil magnate, but unlike other Oil Boom Millionaires, Rockefeller didn’t actually produce any oil. He provided pipeline transfer services to those who did. His company, Standard Oil, was soon “picking up” oil transport contracts and then shipping (or, more to the point, not shipping) oil under transfer agreements wherever Rockefeller wanted it to go, or not go.

This gave J.D. de facto control over the industry. By controlling the transport of oil, he controlled the supply of oil, and that meant he also controlled the price of oil, the availability of oil, and the fortunes of specific oil producers. He was the Middleman, who could facilitate the flow of oil or obstruct the flow of oil at will.

Finally, fed up with the coercive tactics and monopoly practices and obstruction of trade created by Standard Oil, the company was sued and broken up after the Second World War.

What most people don’t yet realize is that Rockefeller did the same exact thing with the banking industry. The Swift System is the equivalent of Standard Oil. Just like what J.D. did with the flow of oil, his sons did with the flow of money— and they did it on a much bigger scale.

J.D. Rockefeller ‘s oil pipelines crisscrossed the entire nation, but his sons’ money pipelines crisscrossed the entire planet, and with much more devastating effects on free trade and the entire world economy.

It is not an accident that the members of the Rockefeller family took the profits and knowledge they gained from the wreck of Standard Oil and reinvested it in the International Monetary Fund as shareholders and founders of the IMF. Nor is it coincidence that the IMF has functioned as the “United States Treasury” since 1924.

Using the excuse of “National Security” the Rockefellers could shut down any business enterprise, simply by cutting off access to money and credit. Just like J.D. shut down oil producers and strangle-held oil supplies for fun and profit.

They haven’t had to prove that the victims actually did anything wrong to exercise this arbitrary power, because Swift is their private system. They can withhold access to Swift services to any individual (bank or other person) at any time for any reason or no reason at all, by invoking their ownership interest.

Just like a restaurant can say, “No shirt, no shoes, no service.” or a drug store can say, “Masks are required in this store.” the Swift System has been able to say, “Tell us where you got your money and who you are sending it to and why you are sending it — or we’ll assume you are up to no good and won’t provide transfer service.”

This gross invasion of banking privacy has put the Rockefellers in the Ultimate Catbird Seat, to know exactly who, what, when, where, and why businesses and individuals are transferring money and credit. They’ve had prior insider knowledge of mergers, resource purchases, investments, borrowing and leveraging, government investigations and everything else impacting specific businesses and entire sectors of the economy, and they’ve been able to sell that knowledge or use it themselves with both impunity and immunity on a worldwide basis ever since the formation of the IMF and the implementation of the Swift System.

This is a hideous invasion of privacy that gives them and their minions-by-default, the banks connected via the Swift System, coercive power over individuals and businesses great and small, and yes, even over the government services corporations that have been functioning “as” governments.

Everyone has to store and move money and credit. That’s the whole point of the world banking system, being able to transfer money from Party A to Party B. It isn’t a complex action, but it is absolutely necessary if you are to buy, trade, or sell anything above the level of barter.

After their success controlling oil supplies, it was a no-brainer to adjust their tactics a little and take over the “money pipelines” in exactly the same way— with the same effect: knowing everyone’s business, exercising monopoly control over transfers, and obstructing trade whenever it suited their interests or the interests of their cronies in Big Business and Government.

Taken in the context of the Big Picture, the Rockefeller’s Swift System has been one of the key instrumentalities of control exercised by both the Federal Reserve and the IMF and all the other Central Banks to manipulate supply and demand of commodities — most especially, money and credit viewed as commodities.

Because the Government Services Corporations acting “as” Governments are required to function on credit by their constitutional contracts, the focus of the banking industry shifted inexorably toward creating more and more and more credit to feed the Government’s insatiable demands.

The asset base available to the banks (their depositor’s money) was exhausted by the 1920’s and even the “Fractional Reserve Banking” racket that allowed them to create ten times the amount of credit compared to the asset base they held in “reserve” was not sufficient.

Besides, the General Public was up in arms about the phony stock market crash of 1929, the Federal Reserve System being implemented, and bank malfeasance in general. Ginning up enough “fresh credit” to keep the Government Corporations happy wasn’t an easy job. In order to do it, the Banks would have to be enabled to claim an ownership interest in more assets.

That’s why they began registering babies in the 1920’s — to claim those babies and their “estates” as “new assets” to use as collateral (“base assets”) to generate more and more and more credit for the use of the Government Corporations and all their franchise corporations— that is, corporations chartered under the US, INC. (Vatican) and the USA, Inc. (British Crown).

This process of coerced and undisclosed registration (Shepherd Townsend Act of 1922), the creation of infant decedent estates resulting from that registration, child labor bonds (Miller Act), and the Buck Act (1940) completed a secret agenda to enslave the assets, including labor assets of Americans, virtually at birth. This unlawful conversion of the child’s political identity allowed the Perpetrators to establish an ownership interest in the child’s body, labor, and anything else they might naturally own as a public or private inheritance.

This created a new asset base owned by the Government Corporations that the banks could use to create up to ten times the asset base in credit for them to loan back to the victims of this outrageous scheme. The Government got unlimited credit, the banks got unlimited usury, the General Public got screwed sideways and upside down.

By the 1980’s even the de facto enslavement of the sleeping Americans and the Europeans and Japanese “captured” in World War II was not enough to feed the need of the banks and the Government Corporations for more credit.

So, they created an “Asset Hamster Mill” —- Platform Trading — to create the appearance of constantly generating and adding new assets to the system, when in fact, they were just recycling the same assets to generate more credit.

Think of it as phony self-generated demand and cash flow, similar to what corporations do when they buy back their own stocks.

In a Platform Trade the owner of actual assets (gold, silver, land, etc.) or someone “representing the owner” — like a Government Services Corporation (CIA) Agent — agrees to lockdown that asset and not use or move it for a specific period of time. The banks then feel confident enough to issue ten times the amount of the asset value as new credit. The banks then kickback an amount of credit equal to the entire value of the asset to the asset owner or their “representative”, and pays the Platform Trader a brokerage fee (anywhere from 10-30% of the total trade) and divides the rest between the asset owner and the other facilitators who issue the actual bonds and buy the stocks and generate the profits that (hopefully) keep this Ponzi Scheme going.

The trust funds and natural resources and labor assets of the Robbed Babies who were victimized in the First Round of the Great Fraud are “locked down” and “taken off-ledger” at the banks to facilitate all this, even though the banks continue to track all these “hidden assets” on different colored screens within the Swift System Database — and these are purportedly invested “for” the “missing” victims of all this chicanery by their purported Trustees — the British Monarch, the Popes, and the Lord Mayors of the Inner City of London.

Of course, the actual owners of the assets being used as collateral “asset reserves” in the Fractional Reserve Banking System, or being locked down to facilitate these Platform Trades, never get a dime. They only get the IRS bills for the Capital Gains Taxes and Estate and Gift Taxes resulting from all this, which they are forced to pay from their own pitiful little earnings.

The Swift System facilitates all this institutionalized theft and graft by transferring or blocking the transfer of the off-ledger assets or the credit resulting from all this clandestine activity, while the members of the “Congress” claiming to “represent” you receive the proceeds owed to you and spend (…. “reinvest”….) it for you in things like taking over other countries, developing bioweapons, weaponizing language, running human trafficking operations worldwide, running huge self-interested propaganda campaigns like the trillion-dollar “Get Vaccinated” BS and the kickbacks to the media corporations, and so on and on.

Beyond all the phony-baloney banking gambits and even beyond all the assets and money and credit that are actually owed to you, beyond the issues of criminality that have to be addressed, there is the problem of how do we keep everyone alive once this nasty bunch of crony corporatists are removed?

The guilty military that is actually responsible for standing by and letting all this happen, and which profited itself grossly in the process (retired military service members —without their knowledge of course — actually own all the Fortune 500 Corporations) has developed the “QFS” — “Quantum Financial System” — in which keystrokes “represent” value, and the digits entered by these precious keystrokes accumulate in imaginary digital “wallets” as “social credits” you can spend.

Of course, they get to control this system, just as the Rockefellers have controlled Swift, and they get to snoop into all business and “personal” transactions, and they get to control how much “social credit” you receive, and dictate where and when you can spend it, and generally, they propose to take over where the Rockefellers left off and impose this coercive new La-La-Land control grid.

The only advantage, and it’s a temporary advantage, is that it is ready to go, and anyone can access its “services” from anywhere in the world.

Can you trust it? No. Is it coercive? Yes. Are those in charge of it trustworthy? Only if you trust the CIA and the corrupt military brass in charge of this whole cluster since 1863.

In terms of cleaning up this whole mess and making a clean board of it, there is exactly one Municipal entity, SERCO, based in Britain, that needs to be taken out. SERCO, which is operated by “the Senior Executive Service” — a bunch of spies and aged bureaucrats steeped in the traditions of the Deep State — is the real lynch-pin, besides Swift, in this whole oppressive system. It bottlenecks progress toward sanity in almost all directions, but it is especially obstructive in that it acts as Paymaster for the U.S. Military.

It’s time we took control of our own military forces and established our own Paymaster, so that we no longer face the specter of foreign powers misdirecting “our” military “for” us and can proceed to do the housecleaning of the political, military, banking, economic, and medical sectors that is necessary.

And then, maybe, finally, we can rejoin the rest of the world as the peaceful, clean, healthy, productive, and happy nation we were prior to the so-called Civil War.

As for our banking system, of, for, and by the people — you can think of the situation this way:

Bank reform had already begun and the banking authorities had already ordered the banks worldwide to become “Basel IV Compliant” — which with a few additions means “Basel III Compliant”. The bank regulators have been losing ground against the coercive powers of Swift for some time now. The plain fact is that Basel III wasn’t honored in any timely fashion, so the regulators issued “Basel IV” to give everyone more time to get in line.

Instead, the managers of Swift saw this as a sign of weakness on the part of the bank regulators and just took advantage of the time extension to create more trouble and more options for themselves —- like the QFS.

Under Basel IV, all the banks are supposed to rework and modernize their transfer capabilities, allowing them to bypass the Swift System if they wish to, and directly interface with other banks via API (Application Programming Interface) and manage their banking relationships directly via RMA (Relationship Management Applications) which are agreements similar to bank treaties.

Obviously, the Swift banks have dragged their feet against this, as it effectively breaks their monopoly and allows banks more privacy and more modern transfer capability.

So now, imagine the situation. You have two pipeline systems laid out on the ground in front of you, one made of old, scabrous red plastic pipe, and a new one made of blue plastic pipe.

The old one is springing leaks and sections of it are being disconnected, while at the same time, the blue pipeline system is not yet all hooked together and fully functional.

Add to this the problem that all countries are not connected to either pipeline system. BRICS, for example, has created its own system to function as a giant private bank to trade in gold and silver and currencies backed by these or other actual assets (like Petrodollars).

The Central Banks and the Commercial Banks that have indulged in all this Bad Faith and Credit Fraud against the interests of the General Public here and abroad are on the ropes, as they should be, and caught between two bad, untenable options — the Swift System and the Quantum Financial System being brought to us by the same military interests that bungled everything up and allowed the Swift System to blossom in the first place.

As a result of all the fraud and deceit and harm done by the Central Banks and the Commercial Banks, some insurance companies are facing bankruptcy and many others are refusing to insure these institutions — for cause. This means that both central banks and commercial banks will be closing by the scores, insurers will be taking it in the shorts, and many of the illegal and undisclosed practices that led to the unjust enrichment of these Schemers are being exposed and shut down.

The entire mortgage industry which was designed to palm off debts owed by defunct bankrupt corporations on living people has to go. The real estate industry which is dependent on an illegally enforced British Land Title Registry system imposed on America has to go. The “Government Agencies” which are subcontractors of our Subcontractor’s Subcontractors have no lawful or legal standing, no authority, and no right to enforce anything against members of the General Public in this country. So they have to go, too.

It seems that there is no good place for the Commercial Banks to go. The U.S. Government has to have credit in order to operate, and corporations worldwide need credit to operate, so there is still a need for Commercial Banks and credit and commercial scrip — stocks, bonds, promissory notes, etc., but, there could be a far better future.

Simply comply with Basel IV, open up the API interfaces that Basel IV provides, and join the Blue Dot Bank System chartered by our actual American Government and organized by the Global Financial Group. Our system is organized so that International Trade Banks own and operate Commercial Bank subsidiaries under the Public Law. It’s transparent for banking customers with regard to their own accounts, but private otherwise, has state of the art IT and interface and transaction capability, and is designed to serve the whole planet.

The entire underlying concept is to make banks honest again, and provide a conduit for the return of assets and credit that is owed to the living people of this planet, one by one by one.

Because there has to be a Debt Jubilee and a Remedy Restitution and a means to deliver the Remedy Restitution to all the individual people who have been harmed by these miscreants, we have designed a banking system for people, not corporations.

So, boot up, compadres. You have skin in this game, whether you knew it or not. And you have a dog in the fight — your own actual Government exercising the powers of an actual Government on your behalf.

If you are in another country, go to our websites to connect to your assemblies. If you don’t yet have a local assembly, or national assembly, representing your country, start one.

The firm, BlackRock Inc., the world’s largest asset manager, invests a staggering $9 trillion in client funds worldwide, a sum more than double the annual GDP of the Federal Republic of Germany.

This colossus sits atop the pyramid of world corporate ownership, including in China most recently. Since 1988 the company has put itself in a position to de facto control the Federal Reserve, most Wall Street mega-banks, including Goldman Sachs, the Davos World Economic Forum Great Reset, the Biden Administration and, if left unchecked, the economic future of our world. BlackRock is the epitome of what Mussolini called Corporatism, where an unelected corporate elite dictates top down to the population.

How the world’s largest “shadow bank” exercises this enormous power over the world ought to concern us. BlackRock since Larry Fink founded it in 1988 has managed to assemble unique financial software and assets that no other entity has. BlackRock’s Aladdin risk-management system, a software tool that can track and analyze trading, monitors more than $18 trillion in assets for 200 financial firms including the Federal Reserve and European central banks. He who “monitors” also knows, we can imagine. BlackRock has been called a financial “Swiss Army Knife — institutional investor, money manager, private equity firm, and global government partner rolled into one.” Yet mainstream media treats the company as just another Wall Street financial firm.

There is a seamless interface that ties the UN Agenda 2030 with the Davos World Economic Forum Great Reset and the nascent economic policies of the Biden Administration. That interface is BlackRock.

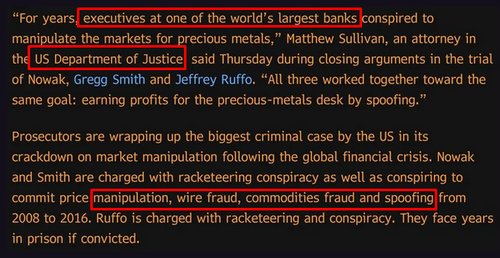

Closing arguments Thursday set the table for years of bank problems. It may be a very serious development. Implications are all laid out clearly in this 9 minute podcast where the DOJ has finally turned its focus on one of the institutions the US has protected for decades. Future implications are very large for bullion banks and executives everywhere. Listen: here.

In the segment we give serious context to the Bloomberg story out late last week on the case. It implies more problems for the bullion banks and their executives down the line. Full 9 minute broadcast here

Points discussed:

US DOJ Accuses JPM Bank of manipulation now

Rogue actors not only ones anymore

Sh*t flows upstream now

Unethical culture is the problem

What it means for Executives

Jamie Dimon, Lloyd Blankfein type of risk

Underlings rolling over on bosses

The many problems surrounding JPM metals

How banks/ funds react to fear

Comex death, Asian birth

Something is going on (Transparency bomb?) between comex drawdowns, JPM case,recategorizing Gold derivatives,and Basel 3

What if a credit card hacker stole your identity and charged a lot of expensive items to your credit card? Would you be obligated to pay for his charges? No.

What if a thief impersonated you, ordered a bunch of supplies for their business on a 30-Day Net Agreement, had the supplies shipped to a warehouse, and then shipped them to Mexico —- skipping town without paying for them. Would you be responsible for this? No.

What if a foreign government said it was involved in salvaging a bankrupt corporation’s assets and charged you a whole bunch of money for service fees and materials to do this “salvage work” when you were never a franchise or shareholder of that corporation? Would you owe any of its debts? No.

These are all examples of “odious debt” — which is strictly defined as dishonest debt and charges related to some kind of scam or fraud scheme from which the victim does not benefit.

In the present situation, the operators of both the US, INC. and the USA, Inc. have profited themselves tremendously at the expense of Americans who have been impersonated as the shareholders and franchises of these corporations— without the nicety of a single dividend check—- and who have had all the expenses of these faceless operators dumped on them with no compensation and no knowledge of what was being done “in their names” at all.

At least $88 Trillion dollars worth of such Odious Debt has been heaped on the American DEBT SLAVES and there is little wonder that some people are staring at this humongous manure pile and talking about “Debt Default” — just telling the rest of the world, sorry, it’s all our fault and we can’t pay, boo-hoo, boo-hoo — which would leave the creditors of the US, INC. and the USA, Inc. free to come in here and take everything as compensation.

No, no, no. What needs to happen is for everyone to wake up and realize that– Number One, no “National Debt” exists, because our equal and answering “National Credit” hasn’t been applied. The books haven’t been balanced. No debt actually exists. By definition.

And Number Two, from our perspective, if any debt remains after National Credit is applied, it’s an Odious Debt having nothing to do with us or our assets. The debt was accrued by foreign commercial corporations hypothecating debt against us while engaged in unauthorized salvage operations on our shores. They used a double-ended impersonation scheme to accomplish this which makes it fraud from the get-go, and so, no, we don’t owe any “National Debt” and any debt that does exist, is Odious Debt associated with foreign commercial corporations. Not us.

One other thing is certain — though we may benefit from the existence of these two foreign corporations in certain respects, we are not the intended beneficiaries of these corporations and we do not receive any juicy corporate dividends or debentures or annuities or any unearned welfare benefits. We are not the owners of these foreign corporations and we are not the owners of any corporation or business or ship that these corporations have legitimately salvaged at any time.

So, no, children, we don’t need to default on a debt that isn’t ours, but the Queen, the Pope, and the Lord Mayor of the Inner City of London, all the British Crown Corporations and all the Municipal Corporations need to pay up for what they have leveraged, squandered, and hypothecated in our names.

—————————-

See this article and over 3700 others on Anna’s website here: www.annavonreitz.com

Government Central Banks were created to control the flow of commodities— and money and credit currencies , like wheat and sow bellies, are commodities. This is state-sanctioned crime, because commodity rigging is a crime—- if Joe Blow does it.

This is why commodity brokers and stock brokers are licensed, too. This is why Central Banks and Stock Exchanges are (supposed to be) regulated.

Merchant banks are created to engage in international trade, which is what we think of as private business between unincorporated entities, using asset-backed money to trade goods and services. It is called “trade” because actual physical assets are being exchanged. My bag of peanuts for your apple is barter; my apple for your silver dime is trade.

Commercial banks deal in various kinds of “commercial paper”—- stocks, bonds, certificates, insurance, debentures, promissory notes and credit instruments such as Letters of Credit, for example. These banks serve incorporated entities since commerce itself is defined as business between two incorporated entities.

Now that you can observe this for yourselves you will better understand it when I say all the commercial banks worldwide are bankrupt and all the central banks are guilty of mammoth crimes beyond the state sanctioned variety crimes they are allowed to indulge in.

As a result, the International Trade Banks are the only ones still standing and capable of translating values. The form this takes does not matter so long as people still have access to abundant cash assets —- without which everyone would be enslaved.

Read that — digital currency is okay so far as it goes— your funds are routinely translated into digits as it is, so it isn’t that digital currency is bad—- it’s that banks controlling the flow of digital currency, banks with the ability to shut down your accounts without agreement, banks that can arbitrarily turn your credit cards on and off, would have complete coercive economic power if we do not immediately and with prejudice insist on maintaining a cash economy wherein people have physical control over defined asset-backed cash currency.

And all this, plus the biggest bust in commodity rigging history and crimes beyond the scope of this quick summation — is what the PTW are arguing and struggling over.

Meantime, note that Goldman-Sachs, the IRS, and the Territorial (British) Federal Reserve have so far moved to China—- obviously planning to set up shop there and do the same things to Chinese workers that they have done here.

Really? Will China be foolish enough to eat the Tapeworms? Stay tuned. We fully intend to take up the criminal nature of these entities with the Chinese Government.

—————————-

See this article and over 3600 others on Anna’s website here: www.annavonreitz.com

Attention: Prosecutor Karim A.A. Kahn,QC; H.E. Joan E. Donoughue, H.E. Kiril Gevgorian, H.E. Cardinal Dominique Mamberti, Lord High Steward Ivan Talbot, Joint Chiefs of Staff, Antonio Guterres Secretary General of the United Nations, Bank of International Settlements, Lord Mayor of Inner City of London, and other Interested Parties:

Consider this lesson in Black Magic to be a necessary part of educating oneself to face off the powers of evil in the modern world.

It’s the end of World War II. Seventeen countries in western and southern Europe teetered on the edge of an Abyss. General George Marshall came up with a Plan to rebuild those countries and their economies and here is how it worked.

A very large amount of privately held gold belonging to the D’Avila Family Trust was “blocked” for fifty (50) years — meaning that the Depositors were denied access to or any ability to move their gold held by banks for a period of fifty years from the date of deposit.

The banks, thus assured of having that gold underwriting their extension of credit promptly issued ten times the value of the gold deposits as credit available to the ravaged countries and their governments under the theory of Fractional Reserve Banking.

Fractional Reserve Banking says, well, on any given day, only about 1/10th of the people will want to take cash out of their accounts, so, we can safely loan out 90% of our “reserves” as credit at interest.

So, in this crazy (and technically illegal) system, the bank gets to create 10X as much credit as the value of the assets that underwrite the bank and keep only the 100% of the gold or other commodity asset, plus 11% of the credit amount as “cash”, to pay off those depositors who at random ask for cash back from their deposits.

The banks are “betting on the margin” in other words and reaping large returns on the interest being paid on these “loans” of credit that is, technically, owed to the heirs of the D’Avila Family Trust and their beneficiaries and not to the banks at all. The banks have nothing at risk and no actual ownership interest in anything.

In 1851 the Spanish Courts ruled that the D’Avila assets came from non-criminal origin and the administrator of the Trust was allowed to deposit these assets in the global banking system. The original agreement for this privilege was for 50 years from the last deposit that happened on October 7th, 1941, so the heir could not remove these assets until October 7th, 1991. The outbreak of World War II changed everything, the United States of America, the Allied Nations, and Non-Allied Nations were seeking a way to rebuild the world after two world wars, the solution was the D’Avila assets. These Assets were transferred to Severino Garcia STA Romana as the asset owner so these assets could be traded for 50 years to fund a global project to rebuild the world. It took some time to plan and position these assets due to World War II and the recovery of assets from Germany and Japan that belonged to the D’Avila Trust. The 50-year agreement was extended to 2005 as the trading of these assets likely did not start until 1955.

All the D’Avila Family Trust assets were placed on deposit as of 1941, so the heirs went hungry to bed for sixty-four years, waiting for 2005 to roll around, and the promised end to the “block” on their funds. They also held the reasonable expectation that at least some of the interest that was collected by the banks would be returned to the Trust, and that they would: (1) be able to enjoy a reasonable standard of living for themselves, and (2) would be able to fulfill the Trust Indenture, which requires the funds to be used to “uplift” humanity.

2005 came and went. More excuses and more shuffling took place. The “arrangement” provided a 5-year window period that extended another five years to 2010, with the understanding that the deposits would finally be released to the control of the heirs and beneficiaries. 2010 came and went. More shuffling. More excuses.

The fact is that the World Bank and IBRD and BIS and all these other banks had grown used to having control of the D’Avila Trust assets secured in their vaults and they had found ways to benefit themselves by manipulating markets and seizing actual physical assets in exchange for loans of “credit” that never even belonged to these banks. All that credit is owed to the Trust, minus reasonable and customary bank and brokerage fees.

By 2005 and 2010, however, it was apparent that the banks couldn’t possibly pay back the D’Avila Trust both the gold and the credit owed from all the interest collected on all those loans, plus keep on glutting themselves, so negotiations came to a standstill. In 2005, the so-called “Off Ledger” — blocked asset accounts, were left in Limbo Land, all the banks and all the governments without a contract to use the gold any longer continued as if they had a contract in place.

What has ensued ever since has been a Bank Club Fest of criminality, greed, unaccountability, lies, and excuses. They all know where the gold that underwrites their banks came from. They all know that the gold assets must be freed up and that the profits from the interest must be shared with the Trust. Most of all, they all know that the accounting is due.

And they are all sitting there, including Karen Hudes, shrugging like so many monkeys, trying to pretend, “Well, hey, this depository account hasn’t been touched in fifty years…. must be “abandoned”….”

That’s their favorite excuse for stealing money, especially money held in Escrow accounts and Slush Funds that the Depositors of the actual assets are never told about.

When you have more than one person, one bank, one agency, one government acting together to prevent the asset owner and/or Heirs from recovering their assets, it is called a conspiracy, a criminal act that has no statute of limitations. Because these assets were placed under Severino Garcia STA Romana as the asset owner and he died in 1974, the assets are protected under an estate with a court appointed Attorney in Fact that has been ordered by the Federal Court of the United States of America to Discover, Collect and Settle the Estate of Severino Garcia STA. Romana. The Claimant against this Estate is the D’Avila Family Trust –the source of the assets deposited by Severino Garcia STA. Romana in the first place.

The actual heir of the D’Avila Family Trust who has the General Power of Attorney for the Trust (there are other heirs, but he holds the GPA) went to Federal Court and to International Courts, and he won his cases to recover these assets from the agencies and banks holding these assets.

The banks are still trying to avoid the judgment in favor of the heirs (STA Romana Family), and claimants (Avila Family) and the actual Beneficiaries — that is, all the people of the Earth.

So, that makes the Banks and everyone protecting the Banks in this matter criminals– unless they immediately Cease and Desist their obstructionist activities and release the D’Avila Depository Accounts and make available the pre-paid credit owed back to the Trust, in recompense for blocking these accounts and extending credit at interest based on these assets since 1941.

How would you feel if you deposited your money in a bank, and that bank arbitrarily blocked your access to your money for eighty years? And then lied about it and said that they don’t know who the Depositor is? That the funds are “abandoned”?

I am the Assign of the D’Avila Trust in my capacity as the Fiduciary for The United States of America, speaking on behalf of the Heirs and Beneficiaries, all living people of this country and ultimately, the planet: it’s time for this criminal nonsense to end, and literally everyone in the world has a stake in helping me to end it.

There are more than 5,000 Family and Institutional Trusts which the banks are attempting to commandeer in this way.

Money is a symbol. Life is the only value. And the debt owed back to the living people is long past due.

The actual ownership interest is known. It has been adjudicated. There is no confusion about it. Not one peso has been “abandoned”. Each bank and each government is responsible and liable.

On the back side of the overall transaction, the interest and return has been paid by living people who didn’t owe the governments that have benefited from the Marshall Plan and the European Economic Recovery Plan a single penny. All that debt was foisted off on individual living people by means of legal chicanery and commercial deceit.

The actual physical assets belonging to families have been seized under conditions of fraud and deceit by banks trading on the assets of the D’Avila Family Trust, in direct violation of the Trust Indenture, which directs this money to be used to uplift humanity and to break the chains of ignorance and poverty.

The banks had the use of the credit generated from the D’Avila Trust assets to use and invest for free, yet they charged rates in usury above 500% on many mortgages that the living people never owed.

These banks have been protected in these outrageous crimes by the members of the Bar Associations, by military contractors, and by politicians who have benefited themselves at the cost of millions of lives, homes, and families.

As I speak, thousands of Americans are being physically evicted from their homes for not paying mortgages that those Americans never owed. Armed thugs acting under color of law have trespassed on private property at the behest of these banks, which are benefiting from the assets of the D’Avila Family Trust and inflicting this crime on the living people that the Trust assets are supposed to help and uplift.

Shame on the Generals who have participated in and allowed this for a cut of the action.

Shame on the Roman Catholic Church and its Collection Agency known as the Internal Revenue Service and the IRS, both, and its venal abusive claim to own the names of living people and to use those names and the assets attached to them as collateral and as the basis of labor contracts without disclosure and without permission.

Shame on the banks and the bankers who have taken such a gross advantage of the D’Avila Family Trust and the Heirs and the intended Beneficiaries of the Trust, with the help of corrupt and incorporated British Crown Corporations that have engineered much of this Crime Against Humanity.

Shame on everyone who has attempted to further block the Heir’s access to their own deposits and to claim that any of these funds are abandoned.

Shame on those who have whipped and beaten and harassed and evicted and stolen the physical assets of the living people using credit and collecting usury based on the use of assets that never belonged to them.

The return on these assets from 153 countries is owed the D’Avila Family Trust and is owed to the intended Beneficiaries of the Trust – which includes all of humanity. Full recompense is due to all the people who have been the victims of the selfishness, trickery, and False Claims in Commerce promoted by these banks.

The Federal Court Order discovery so far has uncovered (below) the banks holding assets covered by the Estate of Severino Garcia STA. Romana. There are still many more banks and accounts holding assets that will be discovered as we continue the discovery as ordered by the Federal Courts:

1. ABN- Amro Bank NV Netherlands (Netherlands, Amsterdam)

2. ABN- Amro Bank Netherlands (Netherlands, Bussum Branch)

3, ABN- Amro Bank Netherlands (Singapore Branch)

4. Agricultural Bank of China (Singapore)

5. Alliance Bank Malaysia Berhad (Kuala Lumpur)

6. Allgemeine Privatkunden Bank (Berlin, Charlottenburg)

7. ANZ Bank Malaysia Berhad (Kuala Lumpur Branch)

8. Arab Bank of Italy (Rome, Italy)

9. Arab Bank of New York (New York)

10. Arab Malaysia Berhad (Kuala Lumpur Branch)

11. Arab Bank PLC (Singapore Branch)

12. Banco Espirito Santo (Lisboa Branch)

13. Banco Central De Resarva De EI Salvador (El Salvador Branch)

14. Bangkok Bank (Kuala Lumpur Branch)

15. Bangkok Bank (Thailand, Bangkok Branch)

16. Bangkok Bank (Hongkong, Main Office)

17. Bangkok Bank Public Company Limited (Singapore Branch)

18. Bank of America National Association (Singapore Branch)

19. Bank of Ayudhya Public Company Limited (Phongpheng Ayudhya Thailand)

20. Bank of Baroda (Bangkok, Thailand)

21. Bank of Canada (Ontario, Canada)

22. Bank of China (Beijing, China Branch)

23. Bank of China (Beijing, main office)

24. Bank of China (Seoul Branch)

25. Bank of China (Shanghai, China)

26. Bank of China (Onsan Branch, Korea)

27 Bank of China (Shanghai & Shenzhen China)

28. Bank of China (Guangdong Branch China)

29. Bank of China (Jakarta Branch Indonesia)

30. Bank of China (Hongkong Branch)

31. Bank of China (Vietnam Branch)

32. Bank of China (Tokyo Branch)

33. Bank of China (Minato, Japan)

34. Bank of China (Singapore Branch)

35. Bank of China (Bangkok, Thailand)

36. Bank of China & Bank of Communication (Guldin Branch, China)

37. Bank of Communications (Singapore Branch)

38. Bank of East Asia Limited (Shenzhen Branch, China)

39. Bank of Estonia (Eesti Pank, Estonia)

40. Bank of Indonesia (Indonesia)

41. Bank of Israel (Israel)

42. Bank of Mongolia (London England Branch)

43. Bank of Japan (Tokyo Head Office)

44. Bank of Negara Malaysia (Kuala Lumpur)

45. Bank of Negara Malaysia (Sarawak Branch, Malaysia)

46. Bank of the Sierra (Porterville, California USA)

47. Bank of Taiwan (Singapore Branch)

48. Bank of Tokyo – Mitsubishi (Hongkong Branch)

49.Bank of Tokyo – Mitsubishi (Tokyo, Japan)

50. Bank of Walnut Creek (Dorville, California USA)

51. Bank of the West (San Francisco, California USA)

52. Bank of, the West (Beverly Hills, California USA)

53.Bank of Yokohama (Hongkong Branch)

54. Bank of Thai Public Company Limited (Bangkok Thailand)

55. Bank of Sierra Leone (Sierra Leone)

56. HypoVereinsbank (Germany)

57. Banco Intesa (Milan, Italy Branch)

58. Barclays Bank (Amsterdam Netherlands)

59. Barclays Bank (Bangkok Thailand)

60. Barclays Banks (Beijing, China)

61. Barclays Bank (Birmingham, U.K)

62. Barclays Bank (Doha, Qatar)

63. Barclays Bank (Dubai, UAE)

64. Barclays Bank (Dublin Ireland)

65. Barclays Bank (Frankfurt, Germany)

66. Barclays Bank (Geneva, Switzerland)

67. Barclays Bank (Hongkong)

68. Barclays Bank (Jakarta, Indonesia)

69. Barclays Bank (Johannesburg South Africa)

70. Barclays Bank (Kuala Lumpur, Malaysia)

71. Barclays Bank (Labuan Malaysia)

72. Barclays Bank (Greater London, England)

73. Barclays Bank (London, England)

74. Barclays Bank (Lausanne, Switzerland)

75. Barclays Bank (Luxemburg)

76. Barclays Bank (Madrid, Spain)

77. Barclays Bank (UK)

78. Barleys Bank (Milan, Italy)

79. Barclays Bank (Moscow, Russia)

80. Barclays Bank (Mumbai, India)

81. Barclays Bank (Paris, France)

82. Barclays Bank (Seoul, Korea)

83. Barclays Bank (Shanghai, China)

84. Barclays Bank (People’s Republic of China)

85. Barclays Bank (Singapore)

86. Barclays Bank PLC (Singapore)

87 Barleys Bank (Sydney, Australia)

88. Barclays Bank (Taipei, Taiwan)

89. Barclays Bank (Tel Aviv, Israel)

90. Barclays Bank (Tokyo, Japan)

91. Barclays Bank (Zurich, Switzerland)

92. BMO Bank of Montreal (Alberta, Calgary, Canada)

93, BMO Bank of Montreal (British Colombia, Canada)

94. BMO Bank of Financial Group. (Toronto, Ontario Canada)

95. BMO Bank of Montreal (Waterloo, Ontario Canada)

96. BMO Bank of Montreal (Quebec, Canada)

97. BMO Bank of Montreal (Nova Scotia, Canada)

98. BNP Paribas (Bahrain Branch)

99. BNP Paribas (Hongkong Branch, Takoo Place Office)

100. BNP Paribas (King Fahd Rd, Kingdom of Saudi Arabia)

101. BNP Paribas (Milano Branch, Italy)

102. BNP Paribas (Rome, Italy Head Office)

103. BNP Paribas Asset Management (Madrid, Spain)

104. BNP Paribas (Singapore)

105. Bulgaria National Bank (Bulgaria)

106. Cassa Di Risparmio Di Ferrara (DI Ferrara, Head Office Italy)

107. Cambodian Commercial Bank (Cambodia Head office)

108. Cambodian Asia Bank (Phnom Penh, Kingdom of Cambodia)

109. Cambodia Asia Bank (Battambang Branch, Cambodia)

110. Cambodia Asia Bank (Siem Reap Branch, Cambodia)

111. CIBC Canadian Imperial Bank of Commerce (Canada)

399. National Bank of Munich (Munich, Switzerland)

400. Credit Suisse Bank (Basle, Switzerland)

401. National Bank of Malawi (Malawi)

402. National Bank of Uzbekistan

403. ING (Amsterdam, Netherlands)

404. Indosuez Bank (Central Hong Kong)

405. Hyakugo Bank (Japan)

406. Deutsche Bank (Germany)

407. FIM Bank Plc. (Malta)

408. Ngan Hang Dong A Eastern Asia Commercial Bank (Hanoi, Vietnam)

409. Vietnam International Bank (Hanoi, Vietnam)

410. Honk Kong Bank (Ho Chi Minh City, Vietnam)

411. Dominion Charter Merchant Ltd. (London, England)

412. Development bank of Japan (Tokyo, Japan)

413. Development Bank of Singapore (Singapore)

414. Daichi Kangyo Bank Limited (Tokyo, Japan)

415. Copenhagen Industrial Bank (Denmark)

416. Central Bank of Argentina

417. Central Bank of Austria

418. Central bank of Brazil

419. Banquo De France (Paris, France)

420. Bank of Israel (Jerusalem, Israel)

421. Bank of Foreign Trade of Vietnam (Ho Chi Mihn City, Vietnam)

422. ANZ Bank (Shanghai, China)

423. ANZ Bank (Seoul, Korea)

424. American Express Bank (Central Hong Kong)

425. Alliance Bank Malaysia Berad (Kuala Lumpur, Malaysia)

426. Agricultural Bank of China (Singapore)

More banks and institutions will be added to this list as the recoupment and discovery progresses. Meantime don’t buy any wooden nickels. There may be Filipinos who are D’Avila family members, and if so, that will be established by blood tests and DNA — not through any claims based on Ferdinand Marcos’ position as a family attorney.

Please bear in mind that although the D’Avila Family Trust is very large, there are other trusts that are also very large that have been arbitrarily encumbered by these miscreants. The V.K. Durham Trust is an American Silver Trust that has been similarly held captive, cheated, and plundered by these criminals. The Guadalupe Hidalgo Treaty Trust Assets have been illegally cashiered by the Bank of England, and the list goes on.

These issues are not unique to America. An estimated ten billion metric tons of gold are owed to the people of Germany and Russia, last seen disappearing into the vaults of the Bank of England.

It is to everyone’s advantage to spread this information far and wide and to bring pressure to bear upon the militaries and the politicians and the banks responsible for this continuing criminality and failure to perform according to our law and custom. Depositors are owed the return of their deposits, otherwise, they would have no reason to deposit any assets with banks in the first place.

Like the institution of government — if a government does not protect you and your assets, it has no valid purpose. A bank that exists to control, encumber, and steal depositor’s money, whether those deposits are small or large, has no valid purpose.

Please join our effort to end this grotesque corruption, end all false claims that the Second World War is in any way unsettled, and demand restoration of private assets to the lawful owners.

You can help me in my role as Fiduciary and Assign overseeing this mess by sharing this information and by properly informing law enforcement and miliary and political leaders as well as bank officers. This has, thus far, been a tremendous effort as the heirs and actual trustees have been left without the means to fight this gigantic theft and fraud.

Put yourselves in their shoes. You are fabulously wealthy, but you live like a serf, and have no money to fight the banks. You want to fund humanitarian projects all over the world and fulfill your ancestors’ dream of “breaking the bonds of poverty and ignorance” but you are prevented from doing this by white collar criminals who use your own assets to pay off other criminals to persecute and intimidate you.

Despite all this, the Heir of the D’Avila Family Trust has won his cases and deserves our support, both in enforcing the law, and on a one-to-one level. It costs money and takes skill and time to prosecute these banks, and at the end of the day, we are left with a piece of paper looking for the enforcement of the court’s orders. We are left to enforce it ourselves, which costs more time, more skills, more money.

Banks need to be regulated. They cannot otherwise be trusted. If the D’Avila Family Trust assets can be stolen by the Bank Mob, why couldn’t yours be stolen, too? Quite aside from the humanitarian and development support that the trust can and will provide each one of us, we all have a vested interest in honest banks and honest business practices. The world cannot long survive or be at peace without these basics in place.

I personally believe that much of the corruption and the violence of the past two hundred years lays at the feet of corrupt banks, corrupt militaries, and corrupt politicians who have undermined proper accounting standards, deregulated the banks and the securities exchanges, and promoted a lawless business environment.

If you are sick and tired of being the goat in this situation, join us. Send your thoughts, your prayers, and any reasonable donation you can make toward ending this to:

Anna Maria Riezinger, In care of: Box 520994, Big Lake, Alaska 99652.

How can we, the living people, tear apart the corporations that are feasting on our bodies, minds, and material assets —-and making a bid to reduce living men and women to the status of animals?

Interestingly, the Pope and the Roman Curia are responsible for defining and regulating all corporations on Earth. That’s why they get a cut of the taxes paid by corporations. Obviously, they are falling down on the job, or they are directly responsible for this latest Tidal Wave of Corporate Criminality, in which case…. holding all those gentlemen accountable would be highly desirable.

You may also remember that the United Nations has historically taken a dim view of Colonialism, but nearly all its member nations have fallen victim to Colonialism’s incorporated Cousin, Territorialism. And they are facing yet another even more oppressive form of the same disease: Regionalism.

Corporatism, or as I call it, “Corporate Feudalism” is the belief that the world would be better off if it were completely controlled by mindless, faceless, unaccountable, and uncontrolled corporations which are single-mindedly motivated by only one goal: profit.

You may have noticed that a basic principle has been breached and that the world of corporations, which is fictional, is somehow bleeding over into the actual world where people live, breathe, and eat and love and fornicate and die. Who is responsible for that breach?

The Pope and his Cardinals and members of the Curia have already been identified and mentioned as part of the problem, but who else?

The Lord Mayor of London, who is in charge of the Magicians known as “twisters” or “attorneys”—- or as our ancestors called them, “Masters of Deceit”. They are the ones who are supposed to be maintaining “the Bar” between fact and fiction, life and corporation.

They are doing a very poor job at the same time that the Pope and the Curia are on strike. In fact, in courts around the world, they are deliberately impersonating living people as CORPORATIONS.

That is, the attorneys are committing crimes of personage, and they are getting away with it.

And who is responsible for that?

Ah, the military and the police and the politicians. The three monkeys and their football.

So what we really need is a “DEFUND” button on the bottom of our computer console, we grab the purse strings back from the politicians, and all this nastiness is over.

But who is giving the politicians access to our money and credit to use against our best interests without our consent in the first place?

The banks.

It all comes down to —- and on —- the banks, because the banks are enabling all this crime.

The Bankers are the Enablers, the Politicians are the Corporate Mouthpieces misdirecting the police and military to take orders from the Attorneys, who are committing crimes of personage against the living people, to enrich the Pope and his pals, the Roman Curia, and all their cronies.

There the condition of the world is, all neatly summarized. We know what’s wrong. We know who is at the bottom of it. Now, what are we going to do about it?

—————————-

See this article and over 3600 others on Anna’s website here: www.annavonreitz.com

Talk of a looming recession is rampant around the globe, and now a major U.S. bank has issued its own dire forecast for the global economy.

It’s been over a month since Russia invaded Ukraine, leading to an unforeseen and prolonged fallout for the global economy. Combined with an inflation problem that was already spiking the prices of virtually every commodity, global institutions have begun ringing the alarm bells that we are on the brink of a long-anticipated recession.

In an investment strategy report sent to clients on Thursday, Bank of America analysts warned that “inflation always precedes recessions” and that tighter monetary policies being put in place to control surging prices make a “recession shock” very likely.

SA Jural Assembly Comment: This is more lamestream media propaganda to roll out the controlled demolition of the financial system for “The Great Reset” folks; firstly, Russia did not invade Ukraine; secondly, the Federal Reserve System is one big fat giant fiat ponzi scheme; and it is artificially manipulated by the banksters; and their 99 year lease has expired in 2012;

The good news is the United People’s Front banking committee is working hard to get the SA people’s bank online within the next week or so; details will be forthcoming soon;

And, our gold, silver and platinum trading platform should also be online in the next month; we have our own alternative great reset by, for and of the people planned; the cabal need slaves but we don’t need the cabal; the people shall govern soon…

All Russian banks already subjected to sanctions will be disconnected from SWIFT, European Commission President Ursula von der Leyen announced on Saturday. The EU, the UK, Canada and the US agreed to implement the measure over Russia’s “special operation” to “de-militarise and de-nazify” Ukraine.

“The removal of Russian banks from SWIFT means that while transactions can continue to take place the means of communicating have been rendered slower,” says Suranjali Tandon, assistant professor at a Delhi-based National Institute of Public Finance and Policy. “In order to predict the impact, it is important to assess the number of banks that currently use SWIFT and the size of transactions undertaken through these.”

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) is a Belgium-based independent organisation that serves as an internal messaging system between over 11,000 banks and financial institutions in over 200 countries. Several major Russian banks, including Sberbank and VTB, could be disconnected from the system in the coming days. The Western leaders have also committed “to imposing restrictive measures that will prevent the Russian Central Bank from deploying its international reserves in ways that undermine the impact of our sanctions.”

Swift logo is placed on a Russian flag are seen in this illustration taken, Bosnia and Herzegovina, February 25, 2022.

Russia’s Vnesheconombank (VEB) stated that having been disconnected from SWIFT, the nation will switch to the financial messaging system (SPFS) of the Russian Central Bank and alternative channels.

“In 2014, Russia had already initiated a switch to its alternative payment system called SPFS,” says Tandon. “To the extent that these banks are used for cross border payments, the impact of the current sanctions will not have the intended impact.”

According to the Central Bank of Russia’s website, at least 331 banks, both domestic and foreign, are listed as the SPFS system users.

“Russia’s withdrawal from SWIFT does not pose a threat to our internal settlements, stimulates the spread of the ruble as an international currency and at the same time reduces the possibility of destructive control by the West of our settlement operations,” Andrey Klimov, head of the Federation Council Commission for the Protection of State Sovereignty, told the press on 27 February.

The Empire is striking back, protecting what really counts, and the Billionaire Bubble sideshow is folding its tents.

One of the most enduring conceits of the modern era is that the Federal Reserve acts to goose growth and therefore employment while keeping inflation moderate (whatever that means–the definition is adjustable). This conceit is extremely handy as PR cover: the Fed really, really cares about little old us and expanding our ballooning wealth.

Nice, except it doesn’t. The Fed’s one real job is defending the U.S. dollar, which is the foundation of America’s global hegemony a.k.a. The Empire.

One thing and one thing alone enables global dominance: being able to create “money” out of thin air and use that “money” to buy real stuff in the real world. The nations that can create “money” out of thin air and trade it for magnesium, oil, semiconductors, etc. have an unbeatable advantage over nations that must actually mine gold or make something of equal value to trade for essentials.

The trick is to maintain global confidence in one’s currency. There is no one way to manage this, as confidence in a herd animal such as human beings is always contingent. Once the herd gets skittish, all bets are off.

In his testimony in early December, U.S. Federal Reserve Chair Jerome Powell admitted it is “probably a good time to retire” the Fed’s characterization of inflation as “transitory”—up, until that time, Powell described inflation as temporary. Today’s guest explains what happens when the Fed “takes away the crutches.” Gerald Celente, the Founder/Director of the Trends Research Institute and publisher of the weekly Trends Journal magazine says, “When interest rates go up, the cheap money flow stops, the economy is going to go down, and the equity markets are going to crash.” In this episode, Gerald shares his 2022 Outlook for: 1. Gold, silver, Bitcoin 2. Commercial real estate 3. U.S. economic front 4. China’s dual-circulation policy 5. The rise of the “Metaverse” Host Robert Kiyosaki and guest Gerald Celente discuss what trends you should be watching in 2022 and how current events both locally and globally will affect your investments. Want three months of the Trends Journal FREE? Get your FREE gift at

This was one of the first educational books we read back in the day to get an innerstanding of how the system actually works; hat-tip to Elizabeth Mary Croft as one of our “freedom from slavery” pioneers;

How is money created? If you ask average people on the street this question, most of them have absolutely no idea. This is rather odd, because we all use money constantly. You would think that it would only be natural for all of us to know where it comes from. So where does money come from? A lot of people assume that the federal government creates our money, but that is not the case. If the federal government could just print and spend more money whenever it wanted to, our national debt would be zero. But instead, our national debt is now nearly 16 trillion dollars. So why does our government (or any sovereign government for that matter) have to borrow money from anybody? That is a very good question. The truth is that in theory the U.S. government does not have to borrow a single penny from anyone. But under the Federal Reserve system, the U.S. government has purposely allowed itself to be subjugated to a financial system in which it will be constantly borrowing larger and larger amounts of money. In fact, this is how it works in the vast majority of the countries on the planet at this point. As you will see, this kind of system is not sustainable and the structural problems caused by such a system are at the very heart of our debt problems today.

Josh Ryan-Collins of the New Economics Foundation explains how banks create money, out of thin air, through the accounting process they use when they make loans.

“Independent Commission on Banking told us that there was a “disagreement” amongst the commissioners about whether or not the banks created money! …So, that’s the situation we’re in. These are the people who are charged with recreating our banking system! And they don’t even understand that banks create credit when they make loans”

The 6 myths about banks and money are:

That banks are intermediaries between savers and borrowers That money is created through the ‘money multiplier’ and the amount of money depends on the amount of ‘base money’ created by the central bank That interest rate adjustments affect bank credit creation That credit allocation is demand driven, rather than controlled by banks That the banks know what’s best for the economy Regulating (or democratising) credit creation doesn’t work.

{kind=link}